SBA Government-backed Loans To Help Small Businesses

SBA loans can seem like a maze of confusing numbers and paperwork, but they’re basically government-backed loans designed to help small businesses, like restaurants, thrive. The Small Business Administration, or SBA, doesn’t actually lend you the money. They’re more like your financial buddy, vouching for you to the lenders.

Restaurants, with their unique set of challenges like seasonality, high overhead costs, and fierce competition, can find a lifeline in SBA loans. These loans aren’t just cash injections; they’re strategic tools to help your restaurant take the next big step, whether it’s expanding your menu, renovating the space, or launching a marketing blitz.

The SBA knows that one size doesn’t fit all, especially in the dining world. That’s why there are specific SBA programs like the 7(a), CDC/504, and Microloan that cater to different needs of restaurant owners. This sort of personalized approach can be a massive game-changer for getting the right kind of support.

Comparing SBA loans to traditional bank loans is like comparing a nicely tailored suit to an off-the-rack one. Sure, traditional loans might be quicker to get, but SBA loans often come with lower interest rates and more flexible terms. This makes them a smart option, especially if you’re playing the long game with your restaurant’s growth.

Types of SBA Loans Suitable for Restaurants

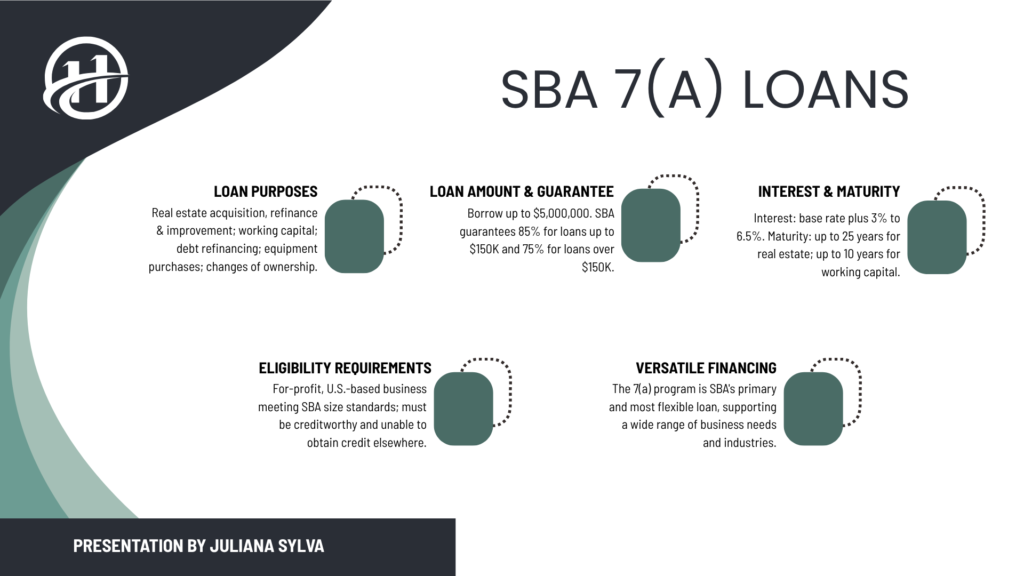

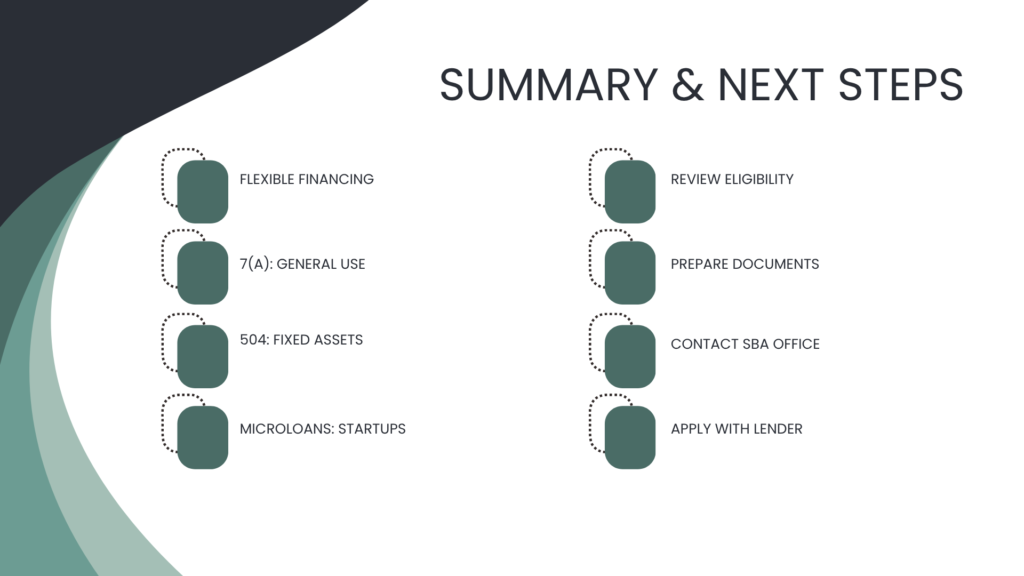

Not every restaurant needs the same type of loan; that’s why the SBA has different options. The 7(a) Loan Program is your workhorse. It’s flexible enough to cover a variety of needs—buying new kitchen equipment, refinancing your debt, or even just having a safety net of cash. It’s like your utility player in baseball, always ready to step in where needed.

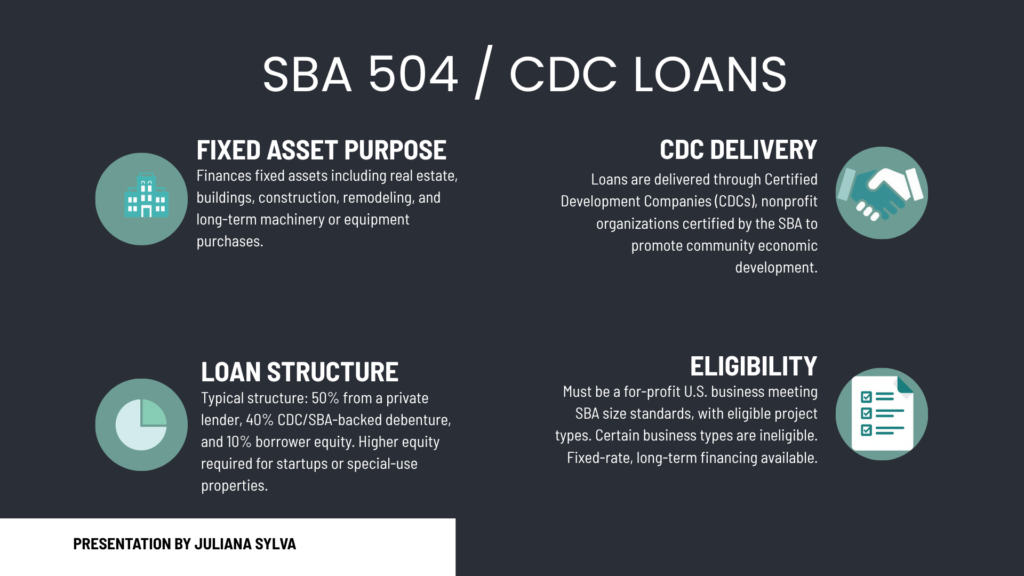

Some restaurant owners might be dreaming bigger, and that’s where the CDC/504 Loan Program comes into play. This one’s all about investing in big ticket items—think purchasing real estate for your dream expansion or upgrading to state-of-the-art kitchen appliances. It’s geared towards long-term stability, a solid cornerstone for your culinary empire.

Then there’s the Microloan Program, which does exactly what you’d expect. It’s perfect for smaller, but equally crucial needs, like stocking up on ingredients for a new menu or handling some immediate repairs. These loans might seem small, but they pack a punch when it comes to keeping your operations smooth.

If your restaurant has ever faced the seasonal roller-coaster or unexpected dips, the CAPLines Program might just be your new best friend. This program helps manage your working capital needs, making sure that when times are tough, you still keep the lights on and the coffee hot.

Each option comes with its own set of benefits and requirements, so the key is identifying what your restaurant needs most, then picking the loan that feels like the right fit for your situation.

Navigating the Application Process: A Step-by-Step Guide

Getting ready for an SBA loan is a bit like preparing for a big test. You need all your financials at your fingertips and a solid business plan that shows you understand both where your restaurant stands and where you want to take it. Your financial documents tell the story of your restaurant, from earnings to expenses, and they need to be as clear as a recipe.

Picking the right loan program is crucial. It’s like choosing the best dish for your restaurant’s menu. You’ve got to consider what each program offers and decide which one aligns best with your goals and needs. Take time to research and maybe even chat with an SBA advisor to make sure you’re pointing yourself in the right direction.

Going through the list of eligibility requirements and necessary documentation is a must. There’s paperwork, sure, but knowing what’s needed ahead of time can make the process smoother. Lenders want to know they can trust you with their money, and having your paperwork squared away helps build that trust.

Boosting your chances of approval involves putting your best foot forward. Running a restaurant is all about managing details, and that skill comes in handy here. Polish up your application by filling in every detail, double-checking your numbers, and making sure everything adds up. Consider practicing your pitch, so when it’s time to discuss your loan request, you’re speaking confidently and clearly.

Remember, the SBA and their lending partners want to see your restaurant succeed. The more organized and prepared you are, the easier it’ll be to convince them that you’re a safe bet.

Managing Your SBA Loan: Best Practices for Restaurant Owners

Once you’ve got your SBA loan in hand, it’s all about using it wisely. Think of it as a stepping stone to elevate your restaurant to the next level. What’s important is to have a game plan. Before spending a dime, prioritize where it makes the most impact—like upgrading crucial kitchen equipment or revamping your dining area to attract new diners.

Paying back your loan isn’t just about meeting the minimum monthly payment. Craft a savvy repayment strategy that fits your cash flow and business cycle. If business is booming, consider paying a little extra to reduce interest over time. If things slow down, knowing you’ve planned ahead can help you stay cool under pressure.

Transparency with your finances and strong organization can’t be overstressed. Keep your records tidy and accessible. This will not only help you manage the loan effectively but’ll also make any future interactions with lenders smoother if you decide to expand further.

Getting insights from those who’ve walked in your shoes can be invaluable. Look for case studies or stories of fellow restaurateurs who have successfully used SBA loans for growth. Learn from their triumphs and missteps—could be eye-opening to see how they’ve navigated similar challenges.

Running a restaurant is no small feat, but with the right financing, you’re setting yourself up for long-term success. That SBA loan is more than money; it’s an opportunity to turn your restaurant dreams into reality.